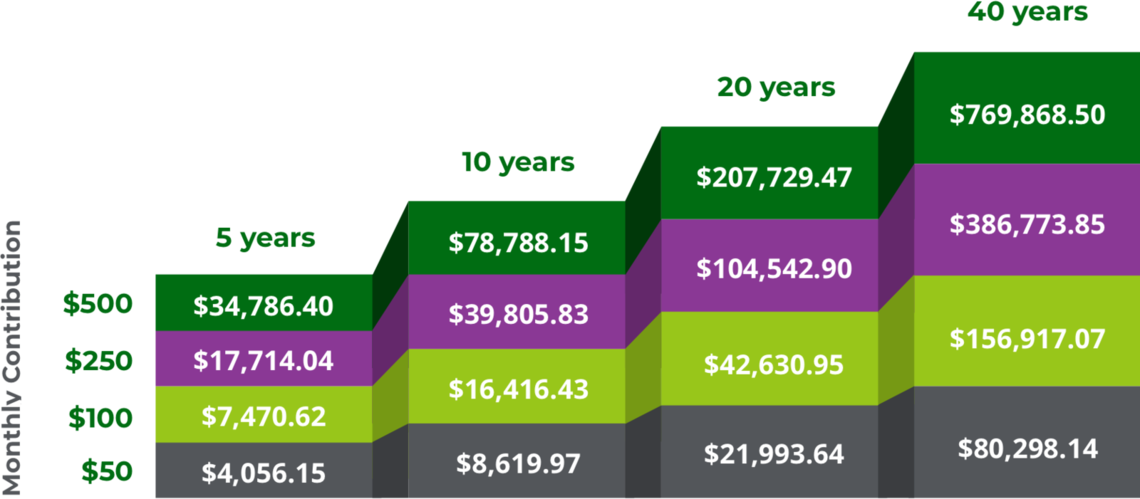

See how your contributions can add up

The standard contribution rate

The default savings rate for a MyCTSavings account is 5% of your gross pay (the amount you earn before taxes), and that amount is deducted from your paycheck after taxes have been taken out.

Change your rate anytime

You can change your savings rate at any time to as little as 1% or up to as much as you want (to a maximum of 100%), within IRS limits. Contributions are made post-tax, and your employer can deduct contributions only from the amount available in your paycheck after other payroll deductions required by law have been made.

Unsure of how much to save?

We have a number of tools and resources to help you plan, as well as our retirement savings calculator. You can also talk to a financial or tax advisor to help you assess your options.

Go to retirement savings calculator

Investments with an assumed 5% annual rate of return*

*This hypothetical example shows the potential of what an initial investment of $500 and a monthly contribution at a 5% projected annual rate of return could become over a period of time. Note this is just an example; your actual results may be more or less.

Contribution limits

Your MyCTSavings account is a Roth IRA, so the total amount you save must be within the federal government’s Roth IRA contribution limits. In 2026, the contribution limits are $7,500 per year to a Roth IRA (and $8,600 per year if you are age 50 or older), as long as you earn at least $7,500 in wages.

The amount of money you can contribute to a Roth IRA depends on how much you earn and your Modified Adjusted Gross Income (MAGI), which is essentially what you earn at your job, plus any other income from investments and other sources. If you file taxes as a single person and your MAGI is under $153K in 2026, or if you are married and file jointly and your MAGI is under $242K, you will be able to contribute the maximum amount of $7,500 ($8,600 if you’re 50 or older). See this IRS publication for more information and an easy-to-follow worksheet for computing your MAGI.